New Economic Thinking

Published on Dec 28, 2014

In a challenge to conventional views on modern monetary and fiscal policy, Professor Bill Mitchell of Newcastle University in Australia has emerged as one of the foremost exponents of Modern Monetary Theory (MMT), a heterodox challenge to the prevailing paradigms which dominate how mainstream economics is taught and economic policy implemented. In his works, and the interview below, Mitchell presents a coherent analysis of how money is created, how it functions in global exchange rate regimes, and how the mystification of the nature of money has constrained governments, and prevented states from acting in the public interest.

Reproduced from: http://bilbo.economicoutlook.net/blog/?p=4870

Stock-flow consistent macro models

Posted on Tuesday, September 8, 2009 by bill

Many readers keep calling for my views on Austrian economics. Apparently when pushing what we might call the Modern Monetary Theory (MMT) view they get hit with a barrage of Austrian school criticism along the lines that statism is dread and that by privatising everything you will improve the human condition. My first thought when I get E-mails like this is to wonder where my readers hang out in their spare time! I wasn’t aware that the Austrian school was anything more than a cobbled together bunch about as large as the modern monetary school (laughing). Anyway, I am taking the request seriously and as a start I present some background – some modern monetary armaments. We are going to war.

The Austrians claim that they predicted the crisis etc is nothing more than recognition that their major hypothesis is that anytime the government is involved in the economy eventually things turn sour. So eventually, given that economic activity cycles, you are going to be correct. However, their understanding of the way the fiat monetary system operates is non-existent. More on the another time.

For now, this blog introduces what is called stock-flow consistent macroeconomic accounting structures. It is based on a paper I wrote last year with James Juniper called There is no financial crisis so deep that cannot be dealt with by public spending.

It is at the pointy end of my blogs and won’t appeal to all. But if you really want to start understanding the quality of modern monetary theory then stock-flow accounting is a good place to start.

What this framework allows you to understand is why the prevailing orthodoxy in macroeconomics has failed. The framework shows you that the mainstream belief that markets self-equilibrate at levels that are remotely socially acceptable is erroneous. Markets do not self-regulate in ways that avoid major financial upheavals and these crises have profound impacts on the real economy.

In particular, the body of literature that is built upon the belief that fiscal policy should only be a passive support to an inflation targeting monetary policy is shown to be highly damaging to the long-term growth prospects of modern monetary economies.

The current crisis confirms that the only way that the non-government sector can save is for the government sector to run continual budget deficits. The stock-flow framework allows you to understand why this fiscal conduct is non-inflationary and, if managed properly, exerts downwards pressure on nominal interest rates and underpins full employment.

To understand how the modern monetary economy operates we need to take a step back into national accounting. First, a modern monetary system has three essential features:

- A floating exchange rate, which frees monetary policy from the need to defend foreign exchange reserves).

- A sovereign government which has a monopoly over the provision its own, fiat currency.

- Under a fiat currency system, the monetary unit defined by the government has no intrinsic worth. It cannot be legally converted by government, for example, into gold as it was under the gold standard. The viability of the fiat currency is ensured by the fact that it is the only unit which is acceptable for payment of taxes and other financial demands of the government.

Within a modern monetary economy, as a matter of national accounting, the sovereign government deficit (surplus) equals the non-government surplus (deficit). The failure to recognise this relationship is the major oversight of neo-liberal (and Austrian) analysis.

In aggregate, there can be no net savings of financial assets of the non-government sector without cumulative government deficit spending. The sovereign government via net spending (deficits) is the only entity that can provide the non-government sector with net financial assets (net savings) and thereby simultaneously accommodate any net desire to save and hence eliminate unemployment.

Additionally, and contrary to neo-liberal (and Austrian) rhetoric, the systematic pursuit of government budget surpluses is necessarily manifested as systematic declines in private sector savings.

The decreasing levels of net private savings which are manifest in the public surpluses increasingly leverage the private sector. The deteriorating debt to income ratios which result will eventually see the system succumb to ongoing demand-draining fiscal drag through a slow-down in real activity. So you have to trace the private indebtedness back to the conduct of the government sector.

The analogy neo-liberals (and Austrians) draw between private household budgets and the government budget is false. Households, the users of the currency, must finance their spending prior to the fact. However, government, as the issuer of the currency, must spend first (credit private bank accounts) before it can subsequently tax (debit private accounts). Government spending is the source of the funds the private sector requires to pay its taxes and to net save and is not inherently revenue constrained.

With that in mind, modern monetary theorists develop a theory of unemployment based on the conduct of fiscal policy (compare that the Austrians who emphasise excessive real wages). In a fiat monetary system, unemployment occurs when net government spending is too low. As a matter of accounting, for aggregate output to be sold, total spending must equal total income. Involuntary unemployment is idle labour unable to find a buyer at the current money wage.

In the absence of government spending, unemployment arises when the private sector, in aggregate, desires to spend less of the monetary unit of account than it earns.

Nominal (or real) wage cuts per se do not clear the labour market, unless they somehow eliminate the private sector desire to net save and increase spending. Thus, unemployment occurs when net government spending is too low to accommodate the need to pay taxes and the desire to net save. This is a fundamental mistake that neo-liberals (and Austrians make).

For example, if you read the classic Austrians, such as Murray Rothbard, you will get this sort of claim in his Power and Market (pages 204-205):

Unemployment is caused by unions or government keeping wage rates above the free-market level.

And this gem from America’s Great Depression (pages 43-44):

Generally, wage rates can only be kept above full-employment rates through coercion by governments, unions, or both. Occasionally, however, the wage rates are maintained by voluntary choice (although the choice is usually ignorant of the consequences) or by coercion supplemented by voluntary choice. It may happen, for example, that either business firms or the workers themselves may become persuaded that maintaining wage rates artificially high is their bounden duty. Such persuasion has actually been at the root of much of the unemployment of our time, and this was particularly true in the 1929 depression.

In a fiat monetary system where the government has currency sovereignty this analysis couldn’t possibly be true. More on this will appear in another blog.

All of the modern monetary propositions can be understood within a flow of funds framework which renders the underlying accounting between flows and stocks consistent. Mainstream economic models do not have stock-flow consistency and therefore fail to understand how the spending relations tie in with the wealth and other stock relations.

Definitions

To understand the difference between a stock and a flow think of a bath-tub. The water in the bath is a stock – it is measured at a point in time. The water that comes into the bath (via the taps) and/or out of the bath (via the sink) are flows and you measure them as a rate of water flow per unit of time. So many litres per minute.

If the inflows are stronger than the outflows the water level in the bath will rise and vice-versa. In other words, flows add to and subtract from stocks.

In economics, this distinction is very important and most students fail to really understand it. I think that is because mainstream macroeconomics then doesn’t go onto to use the distinction properly, especially in the area of fiscal relations.

So the level of bank reserves is a stock – measured at some point each day. Government spending and taxation, consumer spending, saving, investment, exports, imports, etc are all flows of dollars per unit of time. Government spending adds to bank reserves and taxation reduces (drains) the stock of reserves.

Clearly, a theory of the economy that doesn’t recognise the intrinsic relations between the flows and stocks is missing the boat. Given that modern monetary theory is ground out of the operational accounting of the monetary system, its stock-flow consistency is impeccable and unique (a major strength).

A Flow of funds view of modern monetary macroeconomics

A Flow-of-funds approach to the analysis of monetary transactions highlights both the importance of the distinction between and vertical and horizontal transactions and the fundamental accounting nature of the budget constraint identity.

It shows categorically that the Government Budget Constraint (GBC) is an ex post accounting identity rather than an ex ante financial constraint. You will recall that mainstream macroeconomics (and the Austrians) all believe the GBC somehow represents a financial constraint on government prior to it spending.

It doesn’t and cannot in a fiat monetary system unless the government adopts, voluntarily, a framework that replicates the operations of the ex ante GBC. In doing so it reduces its fiscal authority and bows to the pressure of those who oppose government intervention at a sufficient level to generate full employment.

A Flow-of-funds approach also shows that if the sovereign government runs cumulative surpluses which destroy net financial assets then the non-government must accumulate deficits in the form of increasing indebtedness which are unsustainable.

The distinction between vertical and horizontal transactions can be clearly demonstrated by examining the current transactions matrix for a simplified economy.

The last row of the current transactions matrix affords a crucial insight into the nature of (vertical) transactions between the government and non-government sectors.

These transactions must be clearly distinguished from their (horizontal) counterparts: those between banks, households, and firms. The basis for this distinction is that only vertical transactions give rise to net financial assets or increases in real wealth, whereas horizontal transactions net out to zero.

While transaction accounts (or T-accounts) are helpful for distinguishing between such things as high powered money and other forms of money, and for explaining why it makes theoretical sense to consolidate the central banking and treasury functions of government, they are not very helpful when it comes to establishing the difference between vertical and horizontal transactions.

However, this difference can easily be justified by examining a current transactions matrix for the economy, which depicts flows of goods and services and flows of monetary payments between institutions (households, banks, firms, and the government sector).

The following figure is what we call a current transactions matrix and is a highly simplified stock-flow consistent macroeconomic model. I recommend you print the figure by clicking on it and then using the print out it to follow the discussion. Note the -1 or t-1 just means last period’s value.

Here, consumption spending by households, C, comprises wages after tax, W-Tw, plus a fixed share a, of (lagged) household wealth, Vh.

Household wealth increases both through savings out of income, the latter including (lagged) interest receipts on deposits, ib, and dividends received from banks, Fb, and firms, Fd, inclusive of the capital gain on equities (a component subject to minor degree of simplification).

Firm investment is pDK (the D is the greek delta meaning change in), il is the loan rate of interest, and Tl is the tax rate on firm income. It is further assumed that the government chooses the bill rate of interest, ib, tax parameters and government spending as proportion of total capital.

Likewise, it is assumed that firms distribute a fixed share of after tax profits Fd as dividends, while banks distribute their total profits Fb to households. For simplicity, households are assumed to lend all their savings to firms without borrowing themselves.![]()

The sources and uses of funds can be determined by reading the entries in each of the cells in any given column of the matrix.

For the household sector, the sources of funds include wages, interest on deposits, and distributed dividends from banks and firms. Uses of funds include consumption and payment of taxes on household income.

For firms, sources of funds include revenue from the sale of goods and services to households and government, as well as that component derived from the sale capital goods to other firms. These funds are used for investment, the payment of corporate taxes, the payment of interest on borrowings, and the distribution of dividends.

Banks receive interest on loans and issued bank bills, and use their funds for payment of interest on deposits and the distribution of profits.

By summing across the rows for the flow-of-funds accounts of banks, households and firms, it is apparent that all transactions cancel out with the exception of the interest paid on bank bills by government, the payment of taxes by firms and households, and the receipt of revenue by firms for the sale of goods and services to the government.

However, and very significantly, these components are all vertical transactions between the government and non-government sectors. That is they do not net to zero but create/destroy net financial assets in the non-government sector.

Government surpluses must equal non-government deficits

The bottom row of the Current Transactions Matrix indicates that government savings (surplus) or tax revenue net of government spending and payment of interest on bonds ((T – G – ibt-1Bt-1 – 1) are equal to the non-government sector’s dis-savings (deficit = pDK – Fu – Sh).

This is a crucial accounting identity because it implies that, in periods when governments run continual budget surpluses, although economic growth could well be sustained over the short run, this will only happen if the non-government sector runs an on-going deficit, thus accumulating ever-increasing levels of debt.

Moreover, as surpluses destroy net financial assets, this increase in private sector debt will be matched by a continuous decline in net financial assets or wealth.

To show this, we must interpret the flow-of-funds accounts more closely for each of the sectors in terms of how they interact together. However, before this is attempted it is desirable to incorporating transactions with the rest-of-the-world.

Extending the framework to the Rest of the world accounts

The next table is a simplified transactions table which while simplifying the components of GDP, now includes a column for the rest-of-the-world (ROW) account.

Here, Gross Domestic Product, Y, is equal to Private expenditure, PX, plus government expenditure, G, plus exports, X, minus imports, M. The ROW account reveals that imports minus exports and transfers paid by the external sector, TF, equals the balance of payments deficit.

Every item in the Production (GDP) account is matched by a corresponding negative entry in some other column. Taxes net of transfers are received by the government.

Net property income, taxes and transfers, TF and TP, are paid by the external and private sectors, respectively.

The final row totals reveal that public sector net borrowing, PSNB, equals the private net acquisition of financial assets, NAFA (private savings less investment) minus the balance of payments surplus (or plus the deficit), BP.![]() From the perspective of a stock-flow consistent approach to macroeconomic modelling outlined above, the fundamental accounting identity states that government savings (surplus) or tax revenue net of government spending and payment of interest on bonds is equal to the non-government sector;s dis-saving.

From the perspective of a stock-flow consistent approach to macroeconomic modelling outlined above, the fundamental accounting identity states that government savings (surplus) or tax revenue net of government spending and payment of interest on bonds is equal to the non-government sector;s dis-saving.

That is, public sector net borrowing equals the private net acquisition of financial assets (private savings less investment) minus the balance of payments surplus (or plus the deficit). As governments have moved away from deficit spending at levels typical of the post-war period of full-employment, private sector debt levels have escalated.

The reason why this has happened is that causality flows from fiscal policy to the private sector simply because economic influences over the rest-of-the-world account change quite slowly, with income effects dominating over the price effects that are championed by neoclassical theorists.

In contrast, fiscal policy responds immediately to government decisions about spending and taxing. The transmission mechanism behind these changes is complex, as it operates within a portfolio setting, by changing relative rates-of-return between real investment, the equity-premium, and the term structure of bonds.

Sectoral balances

So the framework translates straightforwardly into the familiar sectoral balances accounting relations. They allow us to understand the influence of fiscal policy over private sector indebtedness.

You have seen this accounting identity for the three sectoral balances before:

(S – I) = (G – T) + (X – M)

So total private savings (S) is equal to private investment (I) plus the public deficit (spending, G minus taxes, T) plus net exports (exports (X) minus imports (M)), where net exports represent the net savings of non-residents. That has to hold as a matter of accounting. It is not my opinion.

Thus, when an external deficit (X – M < 0) and public surplus (G – T < 0) coincide, there must be a private deficit. While private spending can persist for a time under these conditions using the net savings of the external sector, the private sector becomes increasingly indebted in the process. For Australia, while the current account deficit has fluctuated with the commodity price cycle, it has continued to deteriorate slightly over the longer term. Accordingly, the dramatic shift from budget deficits to surpluses from the mid-1990s onwards was mirrored by a corresponding deterioration in private sector indebtedness. The only way the Australian economy could keep growing in the period after 1996 was for the private sector to finance increased spending via increased leverage. This is an unsustainable growth strategy. Ultimately the private deficits will become so unstable that bankruptcies and defaults will force a major downturn in aggregate demand. Then the fiscal drag compounds the problem. The solution is simple. The government balance has to be in deficit for the private balance to be in surplus for a stable external balance. In terms of the slightly worsening current account deficit, we can interpret that as signifying an increased desire by foreigners to place their savings in financial assets denominated in Australian dollars. This desire means that that the foreign sector will allow us to enjoy more real goods and services from them relative to the real goods and services we have to export. We note that exports are always a “cost” while imports are “benefits”. As long as there is a foreign desire for our financial assets, the real terms of trade will provide net benefits to Australian residents which manifests as the current account deficit. An external deficit presents no intrinsic problem despite views by the orthodoxy to the contrary. In Japan, by way of contrast, the sectoral balances reveals that the private sector surplus increased on a par with the long-term increase in budget deficits. In other words, the persistent and substantial fiscal deficits financed the saving desires of the private sector and helped to maintain positive levels of real activity in the economy.

Conclusion

This stock-flow accounting structure conditions the way modern monetary theorists think. It is ground in the operational reality of the flow of funds within the economy.

So you cannot possibly say, for example, that the government can run indefinite surpluses while the current account is in deficit, and expect the domestic private sector to be able to save. It has to be that the only way the economy can grow in these circumstances is for the private domestic sector to be increasingly going into debt.

You may think that is fine and we can argue about that as a growth strategy and a reasonable way to manage the need for public goods. That is the debate part. But you cannot deny the former.

The problem is that the Austrians and mainstream economists do deny the accounting statements and demean the rest of their arguments as a consequence. Most of their solutions cannot “add up” in terms of the stock-flow relations.

Enough for now.

Spread the word …

Reproduced from: http://bilbo.economicoutlook.net/blog/?p=332

Deficit spending 101 – Part 1

Posted on Saturday, February 21, 2009 by bill

A lot of people E-mail and ask me to explain why we should not be worried about deficits and why they do not have to be financed by debt (even if the government does typically increase its debt when it goes into deficit). So in the coming weeks I will write some blogs to explain these tricky things. First, I will explain how deficits occur and how they impact on the economy. In particular, we have to disabuse ourselves of the notion that when governments deficit spend they automatically have to borrow which then places pressure on the money markets (which have limited funds available for lending) and the rising interest rates squeeze private investment spending which is productive. This chain of argument is nonsensical and is easily dismissed. So this is Deficits 101. Next time I will detail the reason why the central bank issues bonds (government debt).

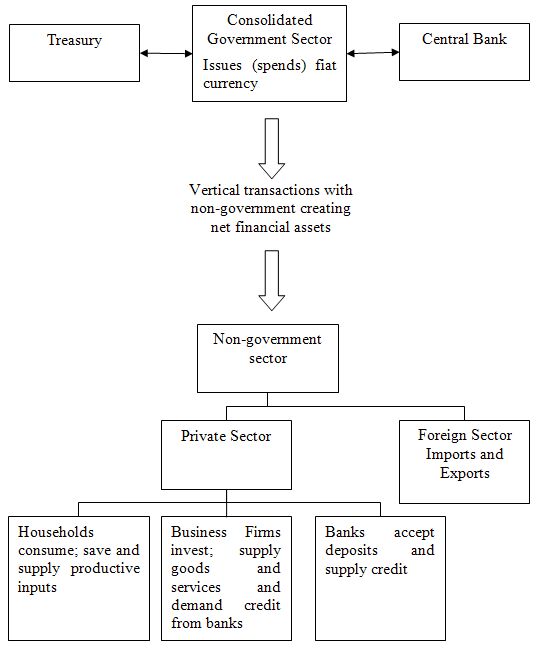

You can use the following diagram to trace through the argument. I suggest you click on it to show it in a new window and then print it and have it beside you as you read the discussion. If you are interested in a more detailed and academic discussion of these issues then I suggest you read my latest book Full employment abandoned: shifting sands and policy failures (with Joan Muysken) which was published by Edward Elgar in 2008. Fiscal deficits or surpluses occur in a modern monetary economies. A modern monetary economy such as Australia and almost every major economy has four essential features:

Fiscal deficits or surpluses occur in a modern monetary economies. A modern monetary economy such as Australia and almost every major economy has four essential features:

- A floating exchange rate, which frees monetary policy from the need to defend foreign exchange reserves;

- Modern monetary economies use money as the unit of account to pay for goods and services. An important notion is that money is a fiat currency, that is, it is convertible only into itself and not legally convertible by government into gold, for instance, as it was under the gold standard.

- The sovereign government has the exclusive legal right to issue the particular fiat currency which it also demands as payment of taxes – in this sense it has a monopoly over the provision its own, fiat currency.

- The viability of the fiat currency is ensured by the fact that it is the only unit which is acceptable for payment of taxes and other financial demands of the government.

The diagram depicts the essential structural relations between the government and non-government sectors. First, despite claims that central banks are largely independent of government, there is no real significance in separating treasury and central bank operations. The consolidated government sector determines the extent of the net financial assets position (denominated in the unit of account) in the economy. For example, while the treasury operations may deliver surpluses (destruction of net financial assets) this could be countered by a deficit (of say equal magnitude) as a result of central bank operations. This particular combination would leave a neutral net financial position. While the above is true, most central bank operations merely shift non-government financial assets between reserves and securities, so for all practical purposes the central bank is not involved in altering net financial assets. The exceptions include the central bank purchasing and selling foreign exchange and paying its own operating expenses. While within-government transactions occur, they are of no importance to understanding the vertical relationship between the consolidated government sector (treasury and central bank) and the non-government sector. We will consider this claim more closely in a future blog.

Second, extending the model to distinguish the foreign sector makes no fundamental difference to the analysis and as such the private domestic and foreign sectors can be consolidated into the non-government sector without loss of analytical insight. Foreign transactions are largely distributional in nature.

As a matter of accounting between the sectors, a government budget deficit adds net financial assets (adding to non government savings) available to the private sector and a budget surplus has the opposite effect. The last point requires further explanation as it is crucial to understanding the basis of modern money macroeconomics.

While typically obfuscated in standard textbook treatments, at the heart of national income accounting is an identity – the government deficit (surplus) equals the non-government surplus (deficit). Given effective demand is always equal to actual national income, ex post (meaning that all leakages from the national income flow is matched by equivalent injections), the following sectoral flows accounting identity holds

(G-T) = (S-I) – NX

where the left-hand side depicts the public balance as the difference between government spending G and government taxation T. The right-hand side shows the non-government balance, which is the sum of the private and foreign balances where S is saving, I is investment and NX is net exports. With a consolidated private sector including the foreign sector, total private savings has to equal private investment plus the government budget deficit.

In aggregate, there can be no net savings of financial assets of the non-government sector without cumulative government deficit spending. In a closed economy, NX = 0 and government deficits translate dollar-for-dollar into private domestic surpluses (savings). In an open economy, if we disaggregate the non-government sector into the private and foreign sectors, then total private savings is equal to private investment, the government budget deficit, and net exports, as net exports represent the net financial asset savings of non-residents.

It remains true, however, that the only entity that can provide the non-government sector with net financial assets (net savings) and thereby simultaneously accommodate any net desire to save (financial assets) and thus eliminate unemployment is the currency monopolist – the government. It does this by net spending (G > T). Additionally, and contrary to mainstream rhetoric, yet ironically, necessarily consistent with national income accounting, the systematic pursuit of government budget surpluses (G < T) is dollar-for-dollar manifested as declines in non-government savings. If the aim was to boost the savings of the private domestic sector, when net exports are in deficit, then taxes in aggregate would have to be less than total government spending. That is, a budget deficit (G > T) would be required.

So how do deficits arise? How does the Federal government spend?

The Federal government has cash operating accounts – to ensure that they can spend (G) on a daily basis and receive daily receipts (T). The Reserve Bank of Australia (RBA) “provides a facility to the Australian Government that is used to manage a group of bank accounts, known as the Official Public Account (OPA) Group, the aggregate balance of which represents the Government’s daily cash position.” (see details here).

When the Federal government spends it debits these accounts and credits various bank accounts within the commercial banking system. Deposits thus show up in a number of commercial banks as a reflection of the spending. It may issue a cheque and post it to someone in the private sector whereupon that person will deposit the cheque at their bank. It is the same effect as if it had have all been done electronically.

All federal spending happens like this. You will note that:

- Governments do not spend by “printing money”. They spend by creating deposits in the private banking system. Clearly, some currency is in circulation which is “printed” but that is a separate process from the daily spending and taxing flows;

- There has been no mention of where they get the credits and debits come from! The short answer is that the spending comes from no-where but we will have to wait for another blog soon to fully understand that. Suffice to say that the Federal government, as the monopoly issuer of its own currency is not revenue-constrained. This means it does not have to “finance” its spending unlike a household, which uses the fiat currency; and

- Any coincident issuing of government debt (bonds) has nothing to do with “financing” the government spending – again this will be explained in a further blog.

All the commercial banks maintain accounts with the RBA which permit reserves to be managed and also allow the clearing system to operate smoothly. These so-called Exchange Settlement Accounts or Reserves always have to have positive balances at the end of each day, although during the day a particular bank might be in surplus or deficit, depending on the pattern of the cash inflows and outflows. There is no reason to assume that these flows will exactly offset themselves for any particular bank at any particular time.

In addition to setting a lending rate (discount rate), the RBA also sets a support rate which is paid on these commercial bank reserves. Many countries (such as Australia, Canada and zones such as the European Monetary Union) maintain a default return on surplus reserve accounts (for example, the RBA pays a default return equal to 25 basis points less than the overnight rate on surplus Exchange Settlement accounts). Other countries do not offer a return on reserves which means persistent excess liquidity will drive the short-term interest rate to zero (as in Japan until mid 2006) unless the government sells bonds (or raises taxes). The support rate becomes the interest-rate floor for the economy. We will investigate this in a further blog.

So Federal spending by the Treasury, for example, amounts to nothing more than the Treasury debiting one of its cash accounts (say by $100m) which means its reserves at the RBA decline by that much and the recipient deposits the cheque for $100m in their private bank and its reserves at the RBA rise by that amount.

Taxation works exactly in reverse. Private bank accounts are debited (and private reserves fall) and the government accounts are credited and their reserves rise. All this is accomplished by accounting entries only. The taxation does not go anywhere! It is not stored anywhere and certainly does not “finance” the spending. The non-government sector cannot pay its taxes until the government has spent! It is a good practice to think of taxes as just draining liquidity from the non-government sector reflecting the Government’s desire for that sector to have less spending capacity.

A simple example helps reinforce these points. Suppose the economy is populated by two people, one being government and the other deemed to be the private (non-government) sector. If the government runs a balanced budget (spends 100 dollars and taxes 100 dollars) then private accumulation of fiat currency (savings) is zero in that period and the private budget is also balanced.

Say the government spends 120 and taxes remain at 100, then private saving is 20 dollars which can accumulate as financial assets. The corresponding 20 dollar notes have been issued by the government to cover its additional expenses. The government may decide to issue an interest-bearing bond to encourage saving but operationally it does not have to do this to finance its deficit. The government deficit of 20 is exactly the private savings of 20.

Now if government continued in this vein, accumulated private savings would equal the cumulative budget deficits. However, should government decide to run a surplus (say spend 80 and tax 100) then the private sector would owe the government a net tax payment of 20 dollars and would need to sell something back to the government to get the needed funds. The result is the government generally buys back some bonds it had previously sold. The net funding needs of the non-government sector automatically elicit this correct response from government via interest rate signals.

Either way accumulated private saving is reduced dollar-for-dollar when there is a government surplus. The government surplus has two negative effects for the private sector:

- the stock of financial assets (money or bonds) held by the private sector, which represents its wealth, falls; and

- private disposable income also falls in line with the net taxation impost. Some may retort that government bond purchases provide the private wealth-holder with cash. That is true but the liquidation of wealth is driven by the shortage of cash in the private sector arising from tax demands exceeding income. The cash from the bond sales pays the Government’s net tax bill. The result is exactly the same when expanding this example by allowing for private income generation and a banking sector.

From the example above, and further recognising that currency plus reserves (the monetary base) plus outstanding government securities constitutes net financial assets of the non-government sector, the fact that the non-government sector is dependent on the government to provide funds for both its desired net savings and payment of taxes to the government becomes a matter of accounting.

Next time I will trace the impact of a budget deficit on the bank reserves and dispel the myths about borrowing and interest rates (that deficits drive up interest rates).

Spread the word …

Reproduced from: http://bilbo.economicoutlook.net/blog/?p=352

Deficit spending 101 – Part 2

Posted on Monday, February 23, 2009 by bill

This is the second blog in the series that I am writing to help explain why we should not fear deficits. In this blog we clear up some of the myths that surround the so-called “financing” of budget deficits. In particular, I address the myth that deficits are inflationary and/or increase the borrowing requirements of government. The important conclusion is that the Federal government is not financially constrained and can spend as much as it chooses up to the limit of what is offered for sale. There is not inevitability that this spending will be inflationary and it does not necessarily require any increase in government debt.

The first thing to recall from Part 1 is that spending by private citizens is constrained by the sources of available funds, including income from all sources, asset sales and borrowings from external parties. Federal government spending, however, is largely facilitated by the government issuing cheques drawn on the central bank. The arrangements the government has with its central bank to account for this are largely irrelevant. When the recipients of the cheques (sellers of goods and services to the government) deposit the cheques in their bank, the cheques clear through the central banks clearing balances (reserves), and credit entries appear in accounts throughout the commercial banking system. In other words, government spends simply by crediting a private sector bank account at the central bank. Operationally, this process is independent of any prior revenue, including taxing and borrowing. Nor does the account crediting in any way reduce or otherwise diminish any government asset or government’s ability to further spend.

Alternatively, when taxation is paid by private sector cheques (or bank transfers) that are drawn on private accounts in the member banks, the central bank debits a private sector bank account. No real resources are transferred to government. Nor is government’s ability to spend augmented by the debiting of private bank accounts.

In general, mainstream economics errs by blurring the differences between private household budgets and the government budget. Statements such as this one from reputed economist Robert Barro that “we can think of the government’s saving and dissaving just as we thought of households’ saving and dissaving” are plain wrong.

Mainstream economics uses the government budget constraint framework (GBC) to analyse three alleged forms of public finance: (1) Raising taxes; (2) Selling interest-bearing government debt to the private sector (bonds); and (3) Issuing non-interest bearing high powered money (money creation). Various scenarios are constructed to show that either deficits are inflationary if financed by high-powered money (debt monetisation), or squeeze private sector spending if financed by debt issue. While in reality the GBC is just an ex post accounting identity, orthodox economics claims it to be an ex ante financial constraint on government spending.

The GBC framework leads students to believe that unless the government wants to print money and cause inflation it has to raise taxes or sell bonds to get money in order to spend. People have the erroneous understanding that taxation and bond sales provide money for the government which they use to spend. So if the government increases its deficit (spending more than taxing) then it must be increasing its debt holdings or “printing money”, both of which are deemed undesirable.

However the reality is far from this erroneous conception of the way the Federal government operates its budget. First, a household, uses the currency, and therefore must finance its spending beforehand, ex ante, whereas government, the issuer of the currency, necessarily must spend first (credit private bank accounts) before it can subsequently debit private accounts, should it so desire. The government is the source of the funds the private sector requires to pay its taxes and to net save (including the need to maintain transaction balances). Clearly the government is always solvent in terms of its own currency of issue.

Mainstream economics also misrepresents what it calls “money creation”. In the popular macroeconomics text, Olivier Blanchard (1997) says that government can also do something that neither you nor I can do. It can, in effect, finance the deficit by creating money. The reason for using the phrase “in effect”, is that … governments do not create money; the central bank does. But with the central bank’s cooperation, the government can in effect finance itself by money creation. It can issue bonds and ask the central bank to buy them. The central bank then pays the government with money it creates, and the government in turn uses that money to finance the deficit. This process is called debt monetization.

This is what mainstream economists call “printing money”. However, it is an erroneous conception in terms of the monetary system. To monetise means to convert to money. Gold used to be monetised when the government issued new gold certificates to purchase gold. Monetising does occur when the central bank buys foreign currency. Purchasing foreign currency converts, or monetises, the foreign currency to the currency of issue. The central bank then offers federal government securities for sale, to offer the new dollars just added to the banking system a place to earn interest. This process is referred to as sterilisation. In a broad sense, a federal (fiat currency issuing) government’s debt is money, and deficit spending is the process of monetising whatever the government purchases.

It is actually rather obvious but all government spending involves money creation. But this is not the meaning of the concept of debt monetisation as it frequently enters discussions of monetary policy in economic text books and the broader public debate. Following Blanchard’s conception, debt monetisation is usually referred to as a process whereby the central bank buys government bonds directly from the treasury. In other words, the federal government borrows money from the central bank rather than the public. Debt monetisation is the process usually implied when a government is said to be printing money. Debt monetisation, all else equal, is said to increase the money supply and can lead to severe inflation.

However, fear of debt monetisation is unfounded, not only because the government doesn’t need money in order to spend but also because the central bank does not have the option to monetise any of the outstanding government debt or newly issued government debt. In Part 3 I will show that as long as the central bank has a mandate to maintain a target short-term interest rate, the size of its purchases and sales of government debt are not discretionary. The central bank’s lack of control over the quantity of reserves underscores the impossibility of debt monetisation. The central bank is unable to monetise the government debt by purchasing government securities at will because to do so would cause the short-term target rate to fall to zero or to any support rate that it might have in place for excess reserves. We will consider this step-by-step in Part 3.

In summary, we conclude from the above analysis that governments spend (introduce net financial assets into the economy) by crediting bank accounts in addition to issuing cheques or tendering cash. Moreover, this spending is not revenue constrained. A currency-issuing government has no financial constraints on its spending, which is not the same thing as acknowledging self imposed (political) constraints.

Once we realise that government spending is not revenue-constrained then we have to analyse the functions of taxation in a different light. Taxation functions to promote offers from private individuals to government of goods and services in return for the necessary funds to extinguish the tax liabilities.

The orthodox conception is that taxation provides revenue to the government which it requires in order to spend. In fact, the reverse is the truth. Government spending provides revenue to the non-government sector which then allows them to extinguish their taxation liabilities. So the funds necessary to pay the tax liabilities are provided to the non-government sector by government spending. It follows that the imposition of the taxation liability creates a demand for the government currency in the non-government sector which allows the government to pursue its economic and social policy program.

This insight allows us to see another dimension of taxation which is lost in mainstream analysis. Given that the non-government sector requires fiat currency to pay its taxation liabilities, in the first instance, the imposition of taxes (without a concomitant injection of spending) by design creates unemployment (people seeking paid work) in the non-government sector. The unemployed or idle non-government resources can then be utilised through demand injections via government spending which amounts to a transfer of real goods and services from the non-government to the government sector. In turn, this transfer facilitates the government’s socio-economics program. While real resources are transferred from the non-government sector in the form of goods and services that are purchased by government, the motivation to supply these resources is sourced back to the need to acquire fiat currency to extinguish the tax liabilities.

Further, while real resources are transferred, the taxation provides no additional financial capacity to the government of issue. Conceptualising the relationship between the government and non-government sectors in this way makes it clear that it is government spending that provides the paid work which eliminates the unemployment created by the taxes.

So it is now possible to see why mass unemployment arises. It is the introduction of State Money (which we define as government taxing and spending) into a non-monetary economics that raises the spectre of involuntary unemployment. As a matter of accounting, for aggregate output to be sold, total spending must equal total income (whether actual income generated in production is fully spent or not each period). Involuntary unemployment is idle labour offered for sale with no buyers at current prices (wages). Unemployment occurs when the private sector, in aggregate, desires to earn the monetary unit of account through the offer of labour but doesn’t desire to spend all it earns, other things equal. As a result, involuntary inventory accumulation among sellers of goods and services translates into decreased output and employment. In this situation, nominal (or real) wage cuts per se do not clear the labour market, unless those cuts somehow eliminate the private sector desire to net save, and thereby increase spending.

So the purpose of State Money is to facilitate the movement of real goods and services from the non-government (largely private) sector to the government (public) domain. Government achieves this transfer by first levying a tax, which creates a notional demand for its currency of issue. To obtain funds needed to pay taxes and net save, non-government agents offer real goods and services for sale in exchange for the needed units of the currency. This includes, of-course, the offer of labour by the unemployed. The obvious conclusion is that unemployment occurs when net government spending is too low to accommodate the need to pay taxes and the desire to net save.

This analysis also sets the limits on government spending. It is clear that government spending has to be sufficient to allow taxes to be paid. In addition, net government spending is required to meet the private desire to save (accumulate net financial assets). From the previous paragraph it is also clear that if the Government doesn’t spend enough to cover taxes and the non-government sector’s desire to save the manifestation of this deficiency will be unemployment. Keynesians have used the term demand-deficient unemployment. In our conception, the basis of this deficiency is at all times inadequate net government spending, given the private spending (saving) decisions in force at any particular time.

For a time, what may appear to be inadequate levels of net government spending can continue without rising unemployment. In these situations, as is evidenced in countries like the US and Australia over the last several years, GDP growth can be driven by an expansion in private debt. The problem with this strategy is that when the debt service levels reach some threshold percentage of income, the private sector will “run out of borrowing capacity” as incomes limit debt service. This tends to restructure their balance sheets to make them less precarious and as a consequence the aggregate demand from debt expansion slows and the economy falters. In this case, any fiscal drag (inadequate levels of net spending) begins to manifest as unemployment.

The point is that for a given tax structure, if people want to work but do not want to continue consuming (and going further into debt) at the previous rate, then the Government can increase spending and purchase goods and services and full employment is maintained. The alternative is unemployment and a recessed economy. It is difficult to imagine that an increasing deficit will be inflationary in a recessed economy because there are so many underutilised resources, both capital and labour.

Indeed, as I continually point out, the first thing that the Federal government should do is offer all the labour that no-one else wants a job and pay them a minimum wage with all the additional statutory entitlements. By definition, the unemployed have no “market price” because there is no demand for their labour. Offering to buy a service for which there is no price is not an inflationary act.

In Part 3, we consider the argument that deficits automatically drive up interest rates because the government borrowing squeezes available funds in the money markets. As you will guess … this is another neo-liberal myth which is designed to render government’s inactive.

Spread the word …

Reproduced from: http://bilbo.economicoutlook.net/blog/?p=381

Deficit spending 101 – Part 3

Posted on Monday, March 2, 2009 by bill

This is Part 3 in Deficits 101, which is a series I am writing to help explain why we should not fear deficits. In this blog we consider the impacts on budget deficits on the banking system to dispel the recurring myths that deficits increase the borrowing requirements of government and that they drive interest rates up. The two arguments are related. The important conclusions are: (a) deficits introduce dynamics which put downward pressure on interest rates; and (b) debt issuance by government does not “finance” its spending. Rather debt is issued to support monetary policy which is expressed as the desire by the RBA to maintain a target interest rate.

In Deficits 101 Part 1 I provided a diagram which depicted the vertical relationship between the government and non-government sectors whereby net financial assets enter and exit the economy. What are these vertical transactions between the government and non-government sectors and what is the importance of them for understanding how the economy works? Here is another related diagram (taken from my latest book Full Employment Abandoned: Shifting sands and policy failures) to help connect the pieces. You might like to click on the picture to get it into a new window and then print it while you read the rest of the text.You will see that this diagram adds more detail to the original diagram from Part 1 which showed the essential relationship between the government and non-government sectors arranged in a vertical fashion.

{kind=link}

Focusing on the vertical train first, you will see that the tax liability lies at the bottom of the vertical, exogenous, component of the currency. The consolidated government sector (the Treasury and RBA) is at the top of the vertical chain because it is the sole issuer of currency. The middle section of the graph is occupied by the private (non-government) sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates the residual (which is in an accounting sense the federal deficit spending) in the form of cash in circulation, reserves (bank balances held by the commercial banks at the RBA) or government (Treasury) bonds or securities (deposits; offered by the RBA).

The currency units used for the payment of taxes are consumed (destroyed) in the process of payment. Given the national government can issue paper currency units or accounting information at the RBA at will, tax payments do not provide the state with any additional capacity (reflux) to spend.

The two arms of government (treasury and central bank) have an impact on the stock of accumulated financial assets in the non-government sector and the composition of the assets. The government deficit (treasury operation) determines the cumulative stock of financial assets in the private sector. Central bank decisions then determine the composition of this stock in terms of notes and coins (cash), bank reserves (clearing balances) and government bonds.

The diagram above shows how the cumulative stock is held in what we term the Non-government Tin Shed which stores fiat currency stocks, bank reserves and government bonds. I invented this Tin Shed analogy to disabuse the public of the notion that somewhere down in Canberra was a storage area where the national government was putting all those surpluses away for later use – which was the main claim of the previous federal regime. There is actually no storage because when a surplus is run, the purchasing power is destroyed forever. However, the non-government sector certainly does have a Tin Shed within the banking system and elsewhere.

Any payment flows from the Government sector to the Non-government sector that do not finance the taxation liabilities remain in the Non-government sector as cash, reserves or bonds. So we can understand any storage of financial assets in the Tin Shed as being the reflection of the cumulative budget deficits.

Taxes are at the bottom of the exogenous vertical chain and go to rubbish, which emphasises that they do not finance anything. While taxes reduce balances in private sector bank accounts, the Government doesn’t actually get anything – the reductions are accounted for but go nowhere. Thus the concept of a fiat-issuing Government saving in its own currency is of no relevance. Governments may use its net spending to purchase stored assets (spending the surpluses for instance on gold or as in Australia on private sector financial assets stored as the Future Fund) but that is not the same as saying when governments run surpluses (taxes in excess of spending) the funds are stored and can be spent in the future. This concept is erroneous. Finally, payments for bond sales are also accounted for as a drain on liquidity but then also scrapped.

The private credit markets represent relationships (depicted by horizontal arrows) and house the leveraging of credit activity by commercial banks, business firms, and households (including foreigners), which many economists in the Post Keynesian tradition consider to be endogenous circuits of money. The crucial distinction is that the horizontal transactions do not create net financial assets – all assets created are matched by a liability of equivalent magnitude so all transactions net to zero. The implications of this are dealt with soon when we consider the impacts of net government spending on liquidity and the role of bond issuance.

The other important point is that private leveraging activity, which nets to zero, are not an operative part of the Tin Shed stores of currency, reserves or government bonds. The commercial banks do not need reserves to generate credit, contrary to the popular representation in standard textbooks.

The central bank operations aim to manage the liquidity in the banking system such that short-term interest rates match the official targets which define the current monetary policy stance. In achieving this aim the central bank may: (a) Intervene into the interbank money market (for example, the Federal funds market in the US) to manage the daily supply of and demand for funds; (b) buy certain financial assets at discounted rates from commercial banks; and (c) impose penal lending rates on banks who require urgent funds. In practice, most of the liquidity management is achieved through (a). That being said, central bank operations function to offset operating factors in the system by altering the composition of reserves, cash, and securities, and do not alter net financial assets of the non-government sectors.

Money markets are where commercial banks (and other intermediaries) trade short-term financial instruments between themselves in order to meet reserve requirements or otherwise gain funds for commercial purposes. In terms of the diagram all these transactions are horizontal and net to zero.

Commercial banks maintain accounts with the central bank which permit reserves to be managed and also the clearing system to operate smoothly. In addition to setting a lending rate (discount rate), the central bank also sets a support rate which is paid on commercial bank reserves held by the central bank. Many countries (such as Australia, Canada and zones such as the European Monetary Union) maintain a default return on surplus reserve accounts (for example, the Reserve Bank of Australia pays a default return equal to 25 basis points less than the overnight rate on surplus Exchange Settlement accounts). Other countries like Japan do not offer a return on reserves which means persistent excess liquidity will drive the short-term interest rate to zero (as in Japan until mid 2006) unless the government sells bonds (or raises taxes). This support rate becomes the interest-rate floor for the economy.

The short-run or operational target interest rate, which represents the current monetary policy stance, is set by the central bank between the discount and support rate. This effectively creates a corridor or a spread within which the short-term interest rates can fluctuate with liquidity variability. It is this spread that the central bank manages in its daily operations.

In most nations, commercial banks by law have to maintain positive reserve balances at the central bank, accumulated over some specified period. At the end of each day commercial banks have to appraise the status of their reserve accounts. Those that are in deficit can borrow the required funds from the central bank at the discount rate. Alternatively banks with excess reserves are faced with earning the support rate which is below the current market rate of interest on overnight funds if they do nothing. Clearly it is profitable for banks with excess funds to lend to banks with deficits at market rates. Competition between banks with excess reserves for custom puts downward pressure on the short-term interest rate (overnight funds rate) and depending on the state of overall liquidity may drive the interbank rate down below the operational target interest rate. When the system is in surplus overall this competition would drive the rate down to the support rate.

The demand for short-term funds in the money market is a negative function of the interbank interest rate since at a higher rate less banks are willing to borrow some of their expected shortages from other banks, compared to risk that at the end of the day they will have to borrow money from the central bank to cover any mistaken expectations of their reserve position.

The main instrument of this liquidity management is through open market operations, that is, buying and selling government debt. When the competitive pressures in the overnight funds market drives the interbank rate below the desired target rate, the central bank drains liquidity by selling government debt. This open market intervention therefore will result in a higher value for the overnight rate. Importantly, we characterise the debt-issuance as a monetary policy operation designed to provide interest-rate maintenance. This is in stark contrast to orthodox theory which asserts that debt-issuance is an aspect of fiscal policy and is required to finance deficit spending.

The significant point for this discussion which we build on next is to expose the myth of crowding out is that net government spending (deficits) which is not taken into account by the central bank in its liquidity decision, will manifest as excess reserves (cash supplies) in the clearing balances (bank reserves) of the commercial banks at the central bank. We call this a system-wide surplus. In these circumstances, the commercial banks will be faced with earning the lower support rate return on surplus reserve funds if they do not seek profitable trades with other banks, who may be deficient of reserve funds. The ensuing competition to offload the excess reserves puts downward pressure on the overnight rate. However, because these are horizontal transactions and necessarily net to zero, the interbank trading cannot clear the system-wide surplus. Accordingly, if the central bank desires to maintain the current target overnight rate, then it must drain this surplus liquidity by selling government debt, a vertical transaction.

The myth of crowding out

We now know that it is a myth to perpetuate the idea that a currency-issuing government is financially constrained. This myth underpins arguments by orthodox economists against government activism in macroeconomic policy. There is another persistent myth that needs to be dispelled – that government expenditures crowd out private expenditures through their effects on the interest rate.

We have seen that the central bank necessarily administers the risk-free interest rate and is not subject to direct market forces. The orthodox macroeconomic approach argues that persistent deficits reduce national savings … [and require] … higher real interest rates and lower levels of investment spending. Think back to the 7.30 Report transcript I provided a couple of days ago.

Unfortunately, proponents of this logic which automatically links budget deficits to increasing debt issuance and hence rising interest rates fail to understand how interest rates are set and the role that debt issuance plays in the economy. Clearly, the central bank can choose to set and leave the interest rate at 0 per cent, regardless, should that be favourable to the longer maturity investment rates.

While we have seen that the funds that government spends do not come from anywhere and taxes collected do not go anywhere, there are substantial liquidity impacts from net government positions as discussed. If the funds that purchase the bonds come from government spending as the accounting dictates, then any notion that government spending rations finite savings that could be used for private investment is a nonsense. A financial expert in the US, Tom Nugent sums it up like this:

One can also see that the fears of rising interest rates in the face of rising budget deficits make little sense when all of the impact of government deficit spending is taken into account, since the supply of treasury securities offered by the federal government is always equal to the newly created funds. The net effect is always a wash, and the interest rate is always that which the Fed votes on. Note that in Japan, with the highest public debt ever recorded, and repeated downgrades, the Japanese government issues treasury bills at .0001%! If deficits really caused high interest rates, Japan would have shut down long ago!

As I have previously explained, only transactions between the federal government and the private sector change the system balance. Government spending and purchases of government securities (treasury bonds) by the central bank add liquidity and taxation and sales of government securities drain liquidity. These transactions influence the cash position of the system on a daily basis and on any one day they can result in a system surplus (deficit) due to the outflow of funds from the official sector being above (below) the funds inflow to the official sector. The system cash position has crucial implications for central bank monetary policy in that it is an important determinant of the use of open market operations (bond purchases and sales) by the central bank.

Here is another diagram that I have drawn to help you put together this part of the argument. You might like to click it to show it in a new window and print it out for reference to make the argument easier to follow. You can see the individual functions of the arms of government are summarised: (a) The Treasury runs fiscal policy which we summarise as government spending and taxation which on any day has some net impact on the economy – either a surplus (G > T) or a deficit (G < T); and (b) The RBA conducts monetary policy through setting an interest rate target. It also has to manage the system-wide cash balances to keep control of its target rate. It does this by selling/buying government debt to influence the reserve positions of the commercial banks. So why does the government issue debt if it is not to finance spending? Well it is rather to maintain these bank reserves such that a particular overnight rate can be defended by the central bank. You can see from the diagram that G adds to reserves and T drains them. So on any particular day, if G > T (a budget deficit) then reserves are rising overall. Any particular bank might be short of reserves but overall the sum of the bank reserves are in excess. In Australia, overnight reserves earn less than the target rate (whereas in some countries they earn nothing). So it is in the commercial banks interests to try to eliminate any unneeded reserves each night. Surplus banks will try to loan their excess reserves on the Interbank market. Some deficit banks will clearly be interested in these loans to shore up their position and avoid going to the RBA’s discount window which is more expensive.

You can see the individual functions of the arms of government are summarised: (a) The Treasury runs fiscal policy which we summarise as government spending and taxation which on any day has some net impact on the economy – either a surplus (G > T) or a deficit (G < T); and (b) The RBA conducts monetary policy through setting an interest rate target. It also has to manage the system-wide cash balances to keep control of its target rate. It does this by selling/buying government debt to influence the reserve positions of the commercial banks. So why does the government issue debt if it is not to finance spending? Well it is rather to maintain these bank reserves such that a particular overnight rate can be defended by the central bank. You can see from the diagram that G adds to reserves and T drains them. So on any particular day, if G > T (a budget deficit) then reserves are rising overall. Any particular bank might be short of reserves but overall the sum of the bank reserves are in excess. In Australia, overnight reserves earn less than the target rate (whereas in some countries they earn nothing). So it is in the commercial banks interests to try to eliminate any unneeded reserves each night. Surplus banks will try to loan their excess reserves on the Interbank market. Some deficit banks will clearly be interested in these loans to shore up their position and avoid going to the RBA’s discount window which is more expensive.

The upshot, however, is that the competition between the surplus banks to shed their excess reserves drives the short-term interest rate down. But, if you understood the discussion above about horizontal transactions (they all net to zero!) then you will appreciate that the non-government banking system cannot by itself (conducting horizontal transactions between commercial banks – that is, borrowing and lending on the interbank market) eliminate a system-wide excess of reserves that the budget deficit created.

What is needed is a vertical transaction – that is, an interaction between the government and non-government sector. In the diagram you will see that bond sales can drain reserves by offering the banks an attractive interest-bearing security (government debt) which it can purchase to eliminate its excess reserves.

That is, the bond sales (debt issuance) allows the RBA to drain any excess reserves in the cash-system and therefore curtail the downward pressure on the interest rate. In doing so it maintains control of monetary policy. Importantly:

- budget deficits place downwardpressure on interest rates;

- bond sales maintain interest rates at the RBA target rate;

Accordingly, the concept of debt monetisation is a non sequitur. Once the overnight rate target is set the central bank should only trade government securities if liquidity changes are required to support this target. Given the central bank cannot control the reserves then debt monetisation is strictly impossible. Imagine that the central bank traded government securities with the treasury, which then increased government spending. The excess reserves would force the central bank to sell the same amount of government securities to the private market or allow the overnight rate to fall to the support level. This is not monetisation but rather the central bank simply acting as broker in the context of the logic of the interest rate setting monetary policy.

Ultimately, private agents may refuse to hold any further stocks of cash or bonds. With no debt issuance, the interest rates will fall to the central bank support limit (which may be zero). It is then also clear that the private sector at the micro level can only dispense with unwanted cash balances in the absence of government paper by increasing their consumption levels. Given the current tax structure, this reduced desire to net save would generate a private expansion and reduce the deficit, eventually restoring the portfolio balance at higher private employment levels and lower the required budget deficit as long as savings desires remain low. Clearly, there would be no desire for the government to expand the economy beyond its real limit. Whether this generates inflation depends on the ability of the economy to expand real output to meet rising nominal demand. That is not compromised by the size of the budget deficit.

Here is a summary of the main conclusions of this blog.

- The central bank (RBA) sets the short-term interest rate based on its policy aspirations. Operationally, Budget deficits put downward pressure on interest rates contrary to the myths that appear in macroeconomic textbooks about crowding out. The central bank can counter this pressure by selling government bonds, which is equivalent to government borrowing from the public.

- The penalty for not borrowing is that the interest rate will fall to the bottom of the corridor prevailing in the country which may be zero if the central bank does not offer a return on reserves, For example, Japan has been able to maintain a zero interest rate policy for years with record budget deficits simply by spending more than it borrows. This also illustrates that government spending is independent of borrowing, with the latter best thought of as coming after spending.

- Government debt-issuance is a monetary policy consideration rather than being intrinsic to fiscal policy; and

- A budget surplus describes from an accounting perspective what the government had done not what it has received.

In short, we should reject any notion that the emerging federal deficits are damaging and will indebt the future generations. The government has chosen to maintain a positive short-term interest rate and that requires the issuance of debt if there are downward pressures on that rate emerging from the cash system. In the next blog in this series Deficits 101 Part 4 I will argue why short-term interest rates should be kept at or around zero, as they are in Japan and the US at present.

Spread the word …